For founders with a PE term sheet

Tiny vs. Private Equity.

What founders actually trade away when they sell to PE — and what they get when they sell to a holding company that holds for the long term.

Short answer

Is Tiny a private equity alternative?

Yes. Tiny is a long-term acquirer for founders who want liquidity without the usual private-equity machinery: fund clocks, required resale timelines, rollover math, debt pressure, and default cost-cutting.

- Tiny's lane: speed, certainty, cash simplicity, team preservation, brand preservation, and long-term ownership.

- PE's lane: competitive headline price, operating discipline, leverage, and a planned exit window.

- Best fit for Tiny: founders who care what happens to the business after close.

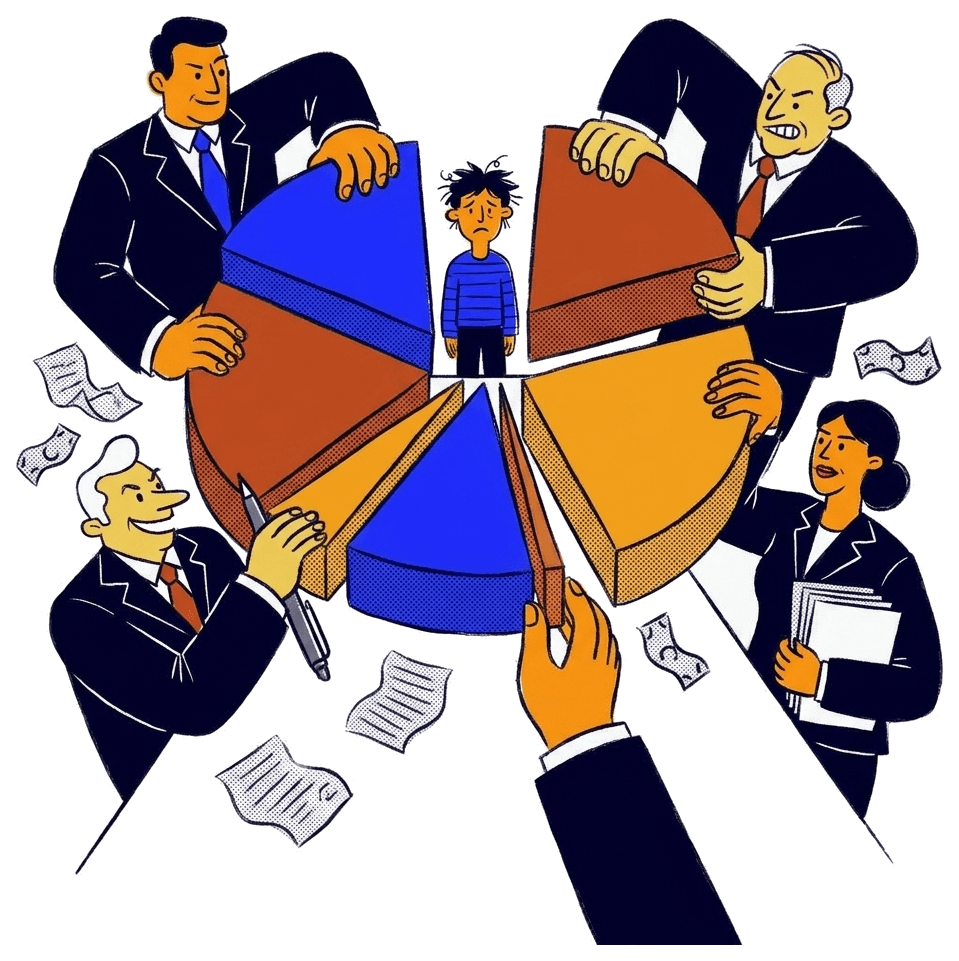

Three buyer profiles, side by side

Most founders are not choosing between good and bad. They are choosing between three kinds of tradeoffs: Tiny, PE, or a strategic buyer. Here is what actually changes after close.

No fund clock

Long-term hold.

Exit required

Usually 3-7 years.

Product absorbed

Usually inside the parent.

No company-level deal debt

We do not load it on.

Debt is normal

It helps finance the deal.

Buyer-dependent

The parent calls the shots.

The team stays

Cuts are common

New finance oversight too.

Overlap gets cut

Duplicate roles disappear.

The brand stays

Often temporary

Kept until the next sale.

Usually absorbed

Or retired outright.

Your call

Stay, step back, or leave.

Plan-driven

Often tied to a plan you did not write.

Earn-out job

Usually 1-2 years.

Cash-heavy at close

Simple structure.

Headline, then math

Rollover, prefs, earn-outs, escrow.

More conditions

Cash, stock, retention packages.

Why founders sell to PE — and why some regret it

Private equity exists because there is a real, valuable thing it does well: it pays a competitive headline price for a profitable business, provides liquidity to founders, and brings operating discipline that a lot of founder-run companies do, in fact, need. For the right asset and the right founder, PE is a perfectly reasonable buyer.

The catch is structural. A PE fund has LPs who expect their capital back, with returns, on a fixed schedule — typically a five-to-seven-year hold inside a ten-year fund life. That clock drives everything downstream: the use of leverage to amplify equity returns, the cost-cutting to lift EBITDA, the tendency to replace the founder if the operating plan demands it, and the inevitable sale to another buyer at the end of the hold.

Most founder regret with PE traces to one of those structural forces. The retrade two months into diligence after the founder is emotionally committed. The earn-out that depended on hitting targets the new owner controlled. The 30-40% layoff in the first ninety days, sold as “synergies.” The CEO replaced inside a year because the original founder was not willing to make the cuts. The dividend recap that left the company saddled with debt and the PE firm with their capital back two years before the exit. None of these are inevitable — but they are choices baked into how PE funds need to operate.

The Tiny model, in plain English

Tiny is a publicly traded holding company that buys profitable businesses and holds them for the long term. Our deals are usually simple and cash-heavy, we do not load the operating company with deal debt, and the brand, team, and roadmap stay intact. For the full story, see our founders page.

Why Tiny can pay competitively despite holding longer

The standard objection to holding long term is that it must mean paying less. That can be true for a fund that has promised its investors they will get their money back on a schedule. The clock forces the buyer to care about how fast it can resell your company.

That is not how Tiny works. We are a public company, and we also use the cash our businesses produce. We are not running on a countdown, and we do not need to sell your company again in a few years to make the deal work. That gives us room to pay a fair price and mean it.

PE offers can look bigger on paper, but the number often shrinks before the founder actually gets paid. Some of it may be tied to staying involved, hitting future targets, or waiting months to see what the buyer decides to release. Our offer is meant to be simpler: the number we agree on is the cash you get when the deal closes.

“The headline number is not what the founder actually receives.”

We walked through the math at tiny.com/blog/pe-math. The short version: every variant of a PE deal — 60% rollover, 80% rollover, or the so-called “100% buyout” — is built around what the PE firm needs to make when it sells again, not how much cash the founder wants to take home.

The real math

What you actually take home

You walk away with $5.5M more by selling to us.

Simple, cash-heavy structures. Done.

A typical PE offer that looks great on paper

Designed to impress you. Here's what you actually get.

In this scenario, you roll 40% equity — PE has a 2x liquidation preference and an 8% annual preferred return. They get paid first.

At least 6 months of lawyers, accountants, and diligence

1-2% fee the PE firm charges your company at closing

Up-front cash in your pocket

What else you give up

- 40% of your company is still locked up — PE can get paid double before you see a dollar

- You report to a new board for 3–7 years

- Major budgets, hires, and strategy changes need their approval

- Monitoring fees get charged to the company during the hold

- 3–6 month process with $500k+ in legal fees

Our offer

Simple terms, fast close, not months of lawyers

Cash in your pocket

What you keep

- Your team keeps their jobs and culture

- You choose your role — stay, advise, or leave

- Earn-outs rare — short and milestone-tied when used. No clawbacks or ratchets in our standard terms.

- No monitoring fees charged back to the company during the hold

- Close on your timeline, as quickly as the business allows

Think selling 80% or 100% to PE is better?

We broke down every PE deal structure — the earn-outs, the preferences, the fees they don't mention until page 47. Almost always worse for the founder.

“I was extremely pleased with how smooth a transition the acquisition was for our team and the community. Zero disruption and a seamless passing of the torch to Tiny.”

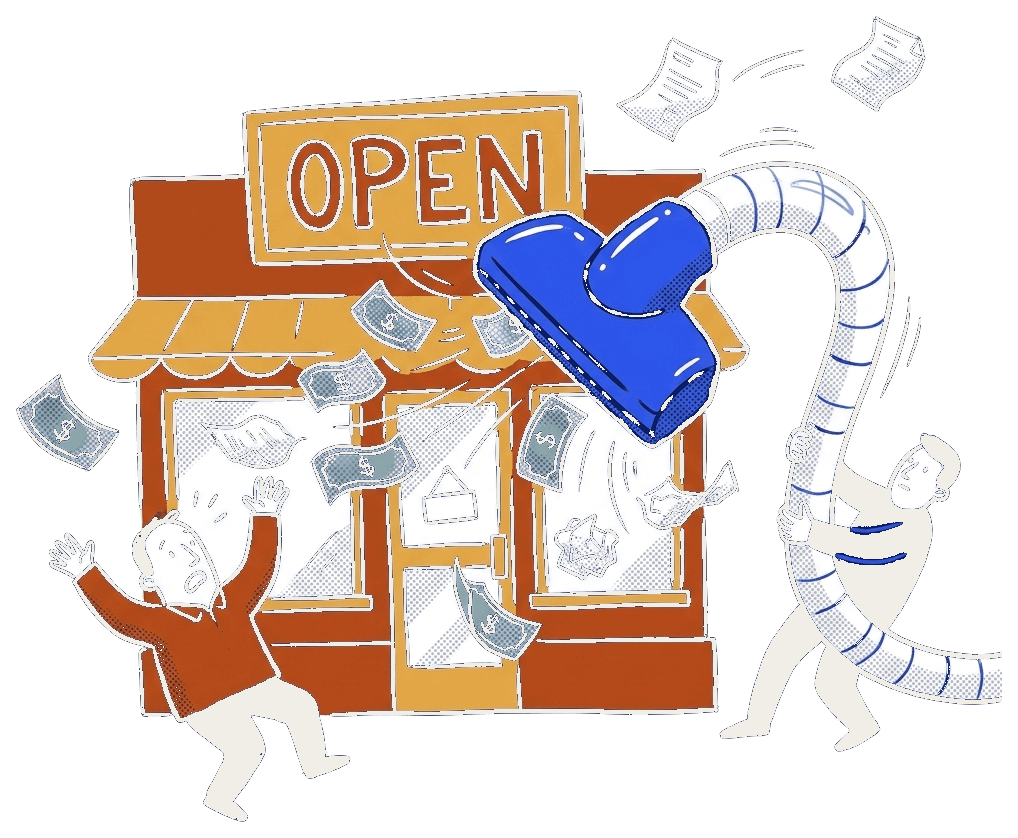

What founders trade away in a PE deal

A PE sale is rarely a single transaction. It is a sequence of decisions the founder no longer makes, each one rational from the fund's perspective and uncomfortable from the founder's.

Debt service

The acquisition debt sits on the operating company. Free cash flow that used to fund product and hiring now services interest.

Operating playbook changes

Costs come out to lift EBITDA. Layoffs are framed as "synergies." The org chart compresses.

Culture and brand

The brand might survive year one; the culture rarely does. Pricing tends to rise. Free tiers tend to disappear.

The founder's continued role

Founder CEOs are often replaced inside 18-24 months if they will not execute the operating plan exactly as underwritten.

The next sale

The exit is already scheduled. In five years your company sells again — to another PE firm, a strategic, or a public-market sponsor — and the team rides another transition.

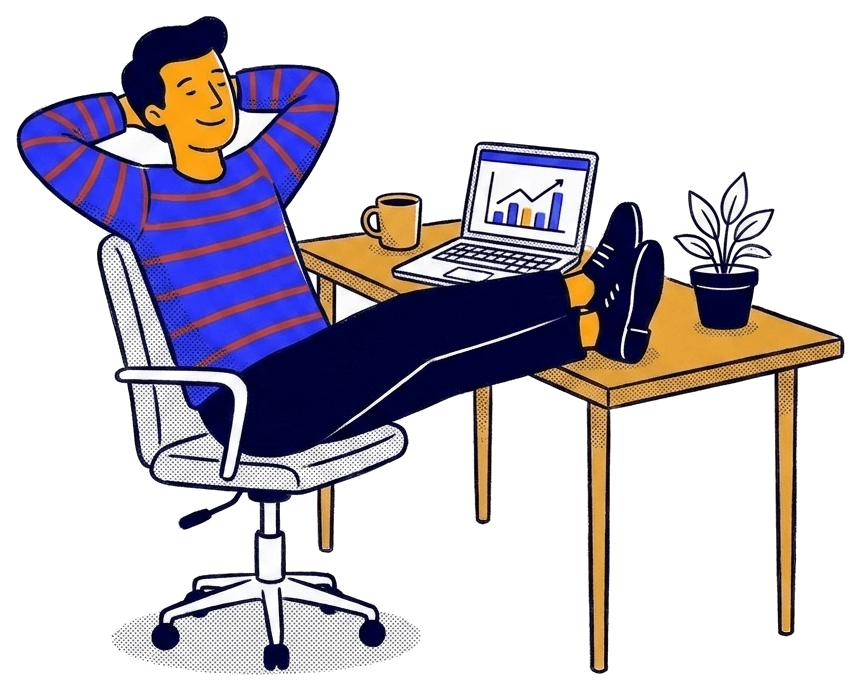

What founders get with Tiny

The mirror image of the list above. Same business, different buyer, different outcomes.

Autonomy

Operating decisions stay with the operator. We do not run a 100-day plan, install our CFO, or schedule quarterly board theater.

Legacy preservation

The brand, team, and roadmap continue. Customers do not get a migration email.

Optional founder role

Stay on as CEO, step into a chair role, or hand it off over 6-12 months. Founder continuity is a feature, not a fail-safe.

Capital allocation help — if you want it

We are good at the financial side of running a portfolio company. If the founder wants help on M&A, debt facilities, or hiring senior finance, we are there. If they do not, we stay out of the way.

No fund clock

No five-year exit window. No LPs to redeem. No fund-driven forced sale.

When PE is actually the right answer

We are not going to pretend Tiny is the right buyer for every company. PE is the right answer in a few specific cases, and founders deserve a fair version of when that is.

- You want the highest possible headline number and you are comfortable with the deal mechanics that come with it.

- The business genuinely needs operational restructuring, and the founder is ready to hand the wheel to a professional operating partner.

- The asset is a roll-up platform — the value creation thesis is consolidation, and PE is the natural buyer for a horizontal roll-up.

- The founder is fully ready to leave on day one and the team is comfortable with a new operating plan within 12 months.

If those describe the situation, PE is a fine answer and we would say so. Tiny is built for the other case — founders who love their business, want liquidity, and want the company to keep thriving long after the sale.

PE-comparison questions founders ask us

Will you load my company with debt after you buy it?

No. We do not load the operating company with the kind of LBO debt private equity uses. Our deals are usually simple and cash-heavy, funded mainly by accumulated free cash flow and patient public-market equity, and any borrowing stays at the holding-company level. The business you sold keeps operating — not a debt-saddled version of it.

Will you sell us again in five years?

Almost never. We hold for the long term. We do not have a fund vintage, an LP base, or a five-year IRR clock. The first business Tiny ever acquired (Metalab, in 2006) is still in the portfolio. That is the model.

Will you replace the management team?

Not as a default. Founders can stay on as CEO, transition out gradually over six to twelve months, or step back at close. We back the operator that is already there unless the founder is ready to leave — in which case we either promote internally or help recruit a successor.

Do you require earn-outs, rollover equity, or hold-backs?

Rarely. Tiny's default is a simple, cash-heavy structure. Earn-outs are uncommon — and when they show up, they are short and tied to milestones we both agree are realistic, not used to defer the purchase price. We do not require rollover equity and do not use a multi-year escrow as a backdoor retrade.

Will my brand change?

No. The brand stays. The team stays. The product roadmap stays under the team that built it. Tiny has 21 companies in the portfolio and they all operate under the brand customers know.

Do you roll up or consolidate portfolio companies?

No. We don't roll up portfolio companies into combined entities. We do not consolidate finance, HR, support, or engineering into a shared service. Each company operates independently with its own team, systems, and P&L.

How is Tiny financed?

Tiny is publicly traded on the Toronto Stock Exchange under the ticker TINY. Our capital comes from public-market equity and accumulated free cash flow from the existing portfolio. We are not a fund. Our investors include Bill Ackman and Howard Marks, who back the permanent-capital model.

How can you compete with PE on price if you hold longer?

Our money is patient and our underwriting is honest. A PE headline number often shrinks once you read the fine print: some money stays in the deal, some is tied to future targets, and some sits in escrow. Our offers are usually simpler and cash-heavy. Once you compare what the founder actually receives, the numbers are closer than the headlines suggest.

Is PE ever the right answer over Tiny?

Yes. If maximizing a headline number is the only goal and you are willing to ride the operational changes, debt service, and a 3-7 year exit window, PE may be a better fit. We are honest about that. Tiny is for founders who want liquidity without trading away the business they built.

What kind of founder is Tiny a good fit for?

Founders who love their business, want liquidity, and want the company to keep thriving after the sale. Founders who would rather their team and customers come out of the deal better off, not worse off. If that sounds like you, email hi@tiny.com.

Curious what the real number looks like?

One call. No pitch deck. Just a founder who's been on your side of the table.

Get a second opinion before you sign