For founders who don't need another round

Tiny vs. Venture Capital.

VC made sense when SaaS multiples were 30x and IPO windows were wide open. That era ended. If your business is already profitable, you don't need to give away 20% per round to find out.

Short answer

Should a profitable founder raise VC or sell to Tiny?

If the business is already profitable and the founder wants liquidity, Tiny can be a cleaner alternative to another financing round: no new dilution, no board reset, no venture-scale outcome requirement, and no need to keep raising to justify the last valuation.

- VC's lane: high-growth companies that need outside capital and can plausibly become fund-returning outcomes.

- Tiny's lane: profitable companies where the founder wants a real exit and a long-term home for the business.

- The question to answer: do you need growth capital, or do you want liquidity and stewardship?

Three paths for a profitable business

If your business is already profitable, VC is no longer the default. You can raise, sell to Tiny, or keep going until PE comes calling. Each path changes who you answer to.

None

You sell once, at your price.

Every round

The cap table keeps changing.

None before sale

Then PE owns it.

No forced exit

Fund timeline

Needs a big exit.

Another sale

Usually 3-7 years.

Sane growth

At the pace the business can handle.

Next-round growth

Fast enough to raise again.

EBITDA growth

Cut what does not help the exit.

Team keeps operating

Approvals add up

Board seats and veto rights.

PE takes control

Operators and quarterly plans.

Your call

Stay, transition, or leave.

Board-dependent

CEO until they decide otherwise.

Earn-out tied

Often 1-2 years.

Cash now

No more dilution.

Maybe huge

Maybe years of dilution.

One sale

Often with rollover or earn-out.

Why VC made sense — and why it often does not anymore

The classic VC bargain is a good one for the right company: capital, network, hiring leverage, and a brand-name term sheet in exchange for ownership, board seats, and IPO-grade growth pressure. It worked extraordinarily well in the 2010s when SaaS multiples were 30x+ revenue and the rocket-ride was real. The companies that took it and made it work are some of the great businesses of the era.

The bargain works less well now, and is a bad fit for most profitable companies in 2026. SaaS multiples normalized. The rocket-ride math broke. The IPO window is narrower than it has been in two decades, and strategic acquirers are pickier. The same Series B that used to be a stepping stone to a $1B+ outcome is now, for many companies, a ceiling — a venture round that demands an outcome the business cannot realistically deliver.

For a profitable business with $3M-$50M in annual profit, the math gets worse with VC, not better. The dilution is real, the growth pressure forces decisions the unit economics do not support, and the path to liquidity narrows to one of two outcomes — an IPO most companies will not reach, or a strategic sale on someone else's timetable.

“The founder ends up owning less of a company optimized for a buyer that may never show up.”

Run the odds before you raise

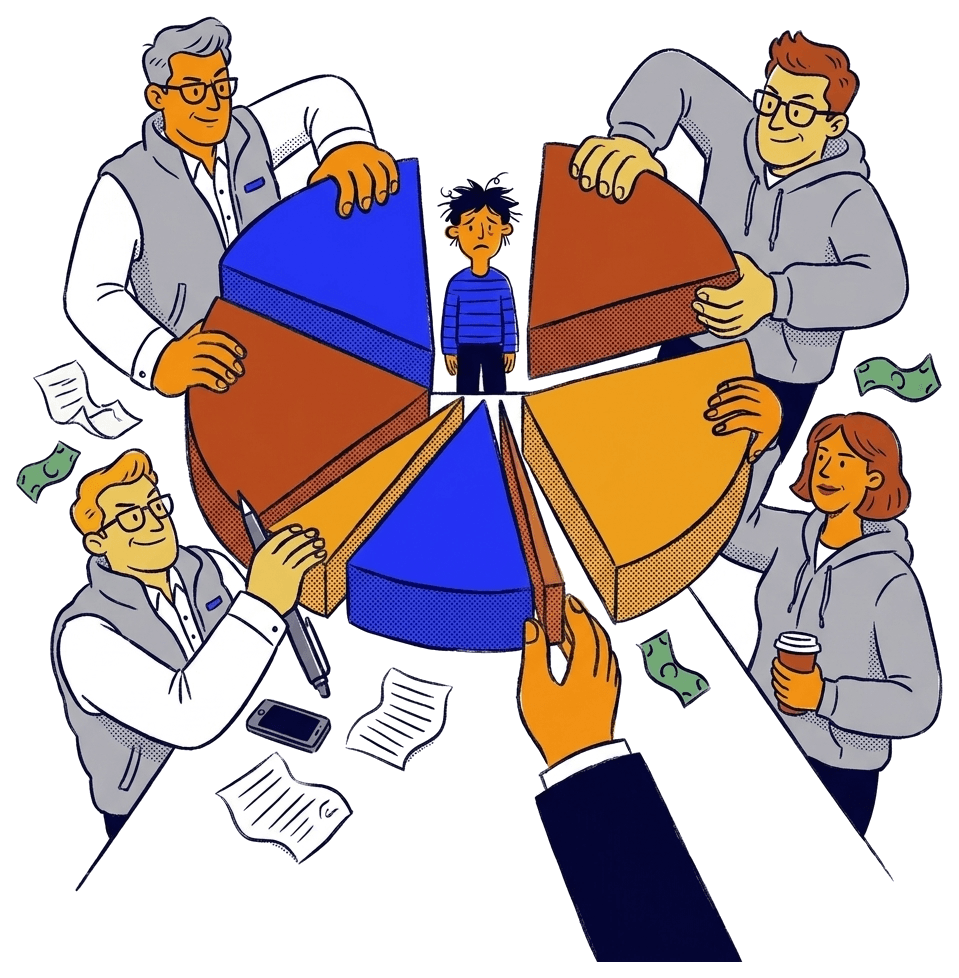

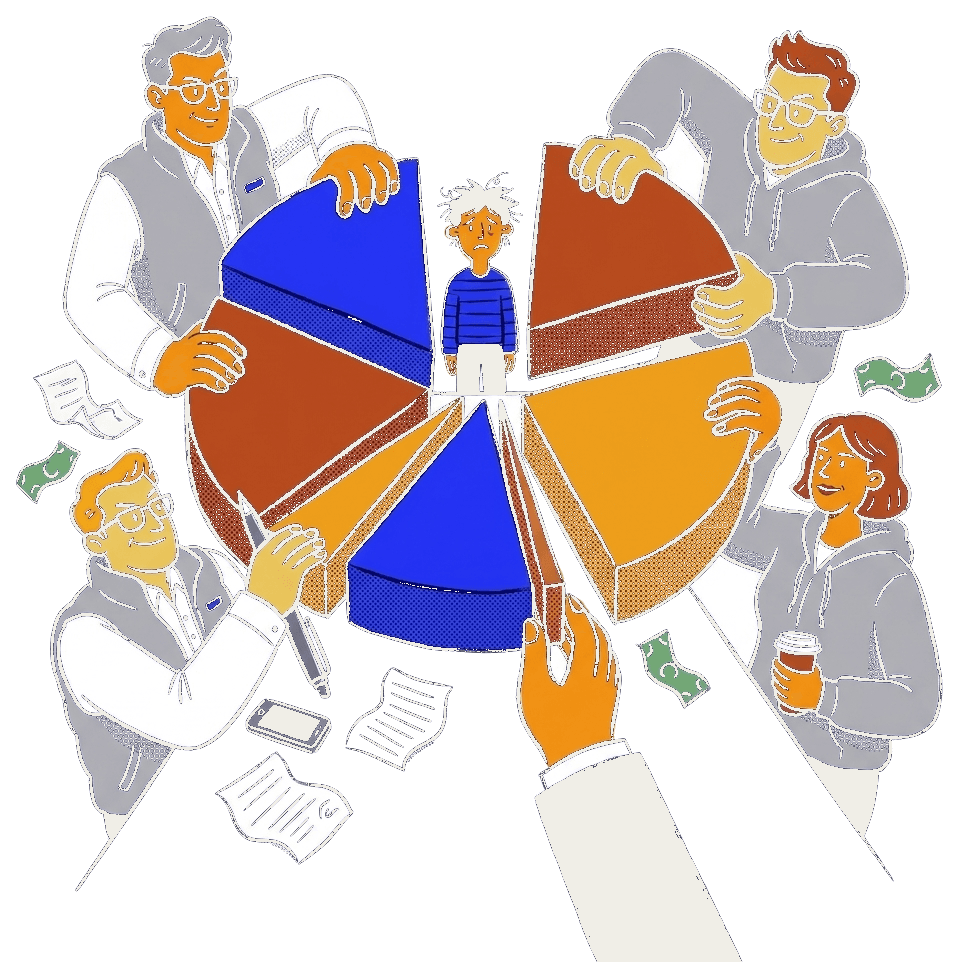

A venture fund makes thirty or forty bets at a time. It needs one of them to return the entire fund. The other thirty-nine can go to zero and the fund still works. That is a good business. It is also their business, not yours. A fund holds a portfolio. You hold one company — the one you are in right now.

Roughly three out of four venture-backed companies never return their investors' money. Most of the rest give back a little. A thin sliver returns almost everything. The entire model is built on that sliver, which is why a healthy company growing 30% a year can read as a disappointment to a board that needed a moonshot.

Stack the rounds and the odds get honest. Of a hundred companies that raise a seed, about half raise a Series A. A handful reach a Series C. One or two have the outcome anyone remembers. Net it out and the chance your equity becomes life-changing money sits in the single digits — before a dollar of preference is paid.

The odds, roughly

- 3 in 4

- venture-backed companies never return their investors’ capital.

- ~1 in 100

- reaches the billion-dollar outcome the whole model is chasing.

- Last

- where your common stock sits at exit, behind every liquidation preference.

That last line is the one founders feel. At the exit, you are last in line. Investors recover their capital first. Raise $40M, sell for $50M, and the headline says success. Once the preference stack clears, the common stock you and your team hold can be worth almost nothing. Valuation is the number in the press release. What clears to you is the number that counts.

Selling to Tiny is not a lottery ticket. It is cash, now, for the company you already built. No preference stack in front of you. No round that has to be raised. No outcome that has to be enormous for yours to be good. You do not need to land in the sliver. You are already in it.

“A fund needs one company in forty to win. You do not have forty companies. You have one.”

What VC takes

A clean way to think about VC is that you trade certainty for optionality. The optionality is real — but the certainty you give up is also real, and it compounds.

Equity dilution

Stepwise across each round. A founder who started at 50% is often well under 15% by the time of an exit.

Board seats and protective provisions

Investor consent becomes required for major decisions — budget, hiring senior leadership, follow-on financing, sale of the company.

Growth-or-die pressure

The fund needs outliers. Anything short of outlier trajectory is a disappointment, even when the business is healthy and profitable.

Exit pressure

Funds have a 10-year life. Year 7 is when the conversation shifts from "how do we grow this" to "how do we get out of this."

Customer outcomes

Pricing rises. Free tiers shrink. Roadmap pivots toward enterprise customers because that is where the next round's multiple lives.

Brand and culture

Both change as the company scales for a venture outcome rather than a durable operating outcome.

The Tiny alternative

Tiny usually buys profitable businesses with a simple, cash-heavy structure and holds for the long term. No dilution, no board seats, no exit clock. For how it works, see our founders page.

“When we ran a process to find a new home for our Meteor business, Tiny moved at lightning speed, kept the terms straightforward, and didn't waste any of our time, which was very different from our experience with some other potential acquirers. We're very happy with how our partnership with Tiny has worked out.”

When VC is still right

We are not going to pretend VC is wrong for everyone. There are real situations where it is the right financing — and the right partner — for the next chapter.

- Winner-take-all markets. Where being second means losing — marketplaces, social networks, parts of infrastructure — capital advantage is real and VC is the right tool.

- Strong network effects or data moats. Categories where scale meaningfully compounds defensibility and a competitor with capital can credibly catch you.

- Capital-intensive scaling. Hardware, biotech, deep tech, or any business that fundamentally needs the capital to operate, not just to grow faster.

- Founders genuinely hunting an IPO outcome. The bargain works if you actually want the public-company path and have an asset that can credibly get there.

For everyone else — profitable businesses with healthy growth, durable economics, and a team that wants to keep building the company they built — Tiny is often the better answer.

What if I already took VC and now want out?

This is the question we get most often from founders who landed on this page. The short answer is yes — we buy VC-backed companies. Creative Market was VC-backed when we acquired it. Meteor had outside investors. Several other portfolio companies came in with cap tables that needed unwinding.

The mechanics are harder. There is a preference stack to clear, a drag-along provision to navigate, board approvals to line up, and investor relationships to manage with care. The deal works when the headline number meaningfully exceeds the preference stack and still leaves a real outcome for common shareholders and the founder team. For a profitable company with reasonable preferences relative to operating value, that math usually clears.

If you are a VC-backed founder reading this — even one with meaningful runway left in the bank — the first call is worth having. We will model the waterfall before either side spends real time on it.

VC-comparison questions founders ask us

Do you buy VC-backed companies?

Yes. Several of our portfolio companies were VC-backed before we acquired them — Dribbble is the best-known example. A clean cap table is easier, but we have closed deals through preferred stacks, drag-along rights, and unspent runway. The process takes longer; it is doable.

What happens to my investors and their liquidation preferences?

They get paid out of the purchase price according to their preferences and the waterfall in your charter. The deal works when the headline number clears the preference stack and still leaves a meaningful amount for common — which it usually does for profitable companies. We will model the waterfall with you before we sign an LOI.

What if we still have meaningful unspent runway in the bank?

Cash on the balance sheet is part of the deal. Either it transfers with the company (and is factored into the purchase price), or it is distributed to investors at close. We work the mechanics with your CFO and counsel. It is a normal part of acquiring a VC-backed company.

What about my unvested stock — will it accelerate at close?

Most plans have single-trigger or double-trigger acceleration on a change of control. We honor whatever your equity plan says. If there is no acceleration, we typically convert remaining vesting into a retention plan at the operating company so key talent stays whole.

We are running an acquihire-style process. Are you in?

Generally no. Acquihires are talent-driven and the customer business is often wound down. Tiny acquires the operating business and keeps it operating. If the product, customers, and economics still make sense as a standalone, we are interested. If only the team is, we are not the right buyer.

Will you let our employees keep their jobs?

Yes. The default is the team stays. We do not run a 100-day plan and we do not consolidate finance, HR, or engineering into a shared service. Each portfolio company operates independently with its own team, systems, and P&L.

What about the founder's continued role?

Optional. Some founders stay on as CEO, some transition out over six to twelve months, and some sell and walk. There is no one right answer — you tell us what you want and we structure the deal around it.

Do you ever invest without acquiring the whole company?

Rarely. Tiny is built to acquire and hold operating businesses, not to write minority cheques. The exception is a small number of strategic minority positions held at the holdco level. The default path for founders is an acquisition, often full or majority, rather than a minority investment.

What size company are you looking for?

Profitable businesses generating roughly $3M-$50M in annual profit, with a defensible product and a team that wants to keep building it. We have acquired companies materially smaller and materially larger; the test is whether the business stands on its own and the team wants to continue.

How is this different from selling to PE?

PE typically loads the company with LBO debt and exits in 3-7 years. Tiny usually uses a simple cash-heavy structure, does not load the operating company with deal debt, and holds for the long term. For the full breakdown see Tiny vs. Private Equity. Both are real options; they answer different founder questions.

Read more

Already profitable? There's a better path than another round.

One call tells you what your business is worth in cash. No dilution. No pitch deck.

Find out what your company is worth